DOL Issues Emergency Extensions to COBRA

The U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) today issued Frequently Asked Questions…

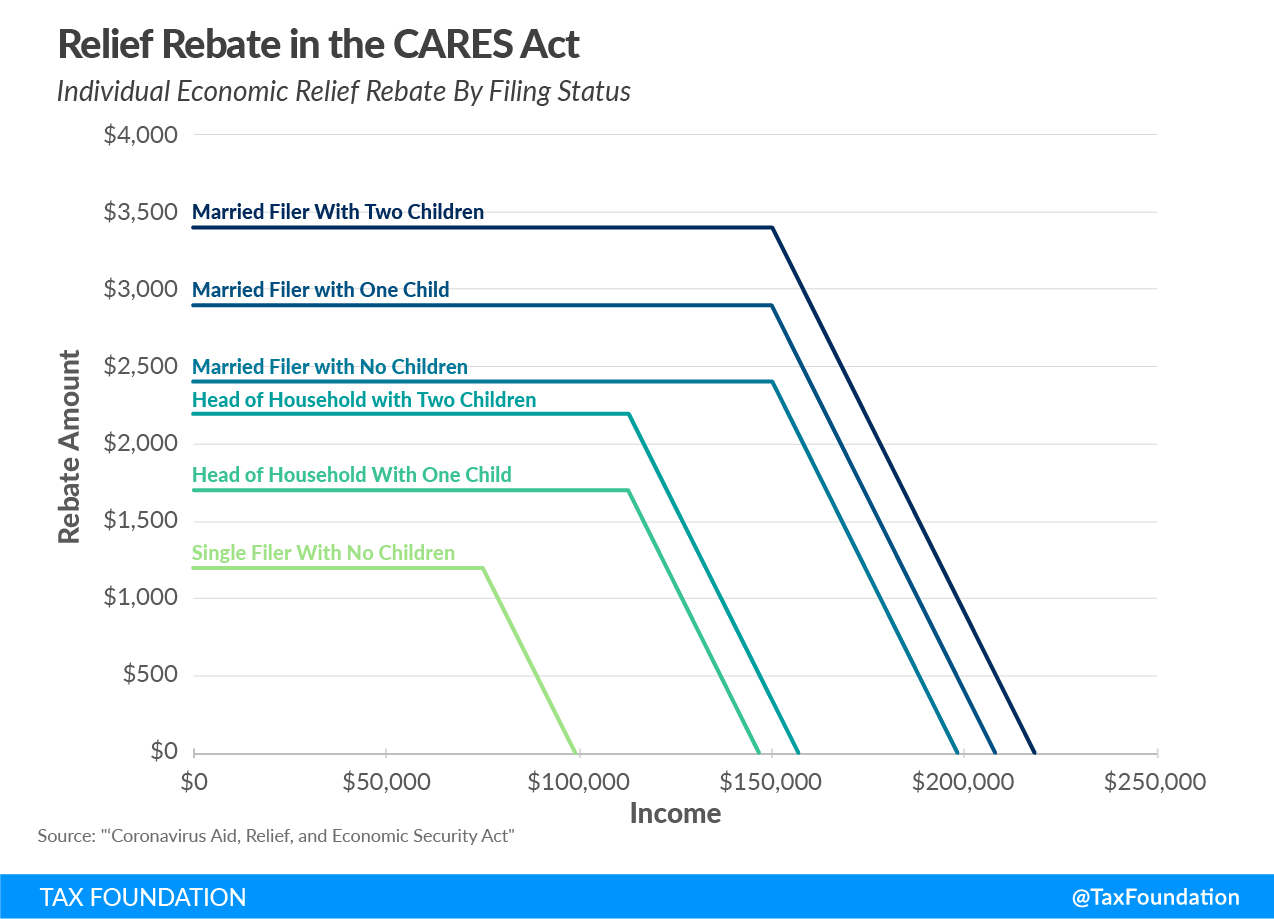

The Coronavirus Aid, Relief and Economic Security Act (CARES Act)

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was signed into law on…

Understanding the $2 Trillion Stimulus Package, Managing Remote Employees and more…

03.27.2020 – Benefits Info COVID-19 Resources Newsletter If you need help understanding the 2 Trillion…

2019 Novel Coronavirus (COVID-19) FAQ UPDATED 3.24.2020

This UPDATED FAQ covers the general topic of COVID-19 virus to explain how various insurance…

2019 Novel Coronavirus (COVID-19) FAQ

03.24.2020 – Please see our updated FAQ for additional guidance, as it pertains to COVID-19.…

Frequently Asked Insurance Questions When Buying A Business

When buying a business, it is important to be aware of any potential insurance challenges…

End of content

End of content

Insurance made simple.

Our newsletters deliver the insights you need to navigate the complexities of insurance.